Colleges and universities in Jiangsu welcome new students one after another, and the class of 2024 "Meng Xin" opens a new journey.

Original title: Jiangsu colleges and universities welcome new students one after another, and the class of 2024 "Meng Xin" opens a new journey-

University, here we come!

On August 24th, more than 4,000 freshmen from all over the world became "Dongda people". Photo by Li Liu

Since August 23, many universities in Jiangsu have ushered in the "Meng Xin" in 2024. The old campus with rich background and the new campus with new appearance are full of vitality. When the freshmen step into the campus with their bags and longings, at this moment, it is both a dream come true and a new beginning.

Go to your alma mater together, and strive for youth to meet here.

What’s it like to be alumni with mom and dad? At the scene, some new students visited the campus with their parents who had studied and lived in the same school.

"My father is more familiar with the Gulou Campus than I am. I live in Room 2 of Taoyuan, and he lived in Room 12 of Nanyuan." On the morning of 24th, in the Gulou Campus of Nanjing University, Ruiqi Luo from Korla, Xinjiang, took a walk with his father on campus as soon as he cleaned up his dormitory. "My father is a Nantah native. He has been telling me about Nantah since he was in primary school. Since then, I have had the desire to apply for NTU. " When volunteering, Ruiqi Luo chose NTU Intelligent System Integration Experimental Class without hesitation. In 1990, after graduating from the School of Earth Science and Engineering of Nanjing University, Luo Dad chose to return to Xinjiang to join the construction of the western region. After returning to his alma mater many years later, Mr. Luo and his son "searched for roots" in the Gulou campus. "I am in the northwest and my heart is in Nantah. I hope that children can study hard in Nantah and become pillars of society! "

"This is Dongda Auditorium, which is the former Institute of Technology. We used to study in the evening here …" On the 24th, Hu Yonghua, who returned to her alma mater, introduced her daughter Hu Xiaoyu incessantly. He and his wife Zhu Ping are both alumni of Southeast University, and their daughter was admitted to the "English+Information Engineering" double-degree major this year. Coincidentally, Xu Jingheng, who studied in Nanjing No.29 Middle School with Hu Xiaoyu, was also admitted to this major, while Jamlom’s parents were alumni of Southeast University majoring in management science and engineering and regional economics in 2002.

Returning to the campus with the children again, Xu Jingheng’s parents also recalled the lush years of that year. "At that time, I lived in Room 9, Wenchang, Sipailou Campus, and my wife’s dormitory was behind Liuyuan Hotel. At that time, I rode my bike from east to west with egg cakes to bring her breakfast every day …" Xu Dad said, smiling hard on his face. Xu Jingheng, who grew up listening to the "omelet story", designated Dongda as an ideal university in his freshman year of high school and kept fighting for it. "What touches me most is the unique cultural atmosphere of Dongda University. I hope to make more friends here and become a better self." Xu Jingheng said.

Go back to the old campus to "seek roots" and go to the new campus to dream.

Since Nanjing University started its "root-seeking school" in 2022, all the freshmen in the school have stayed in Gulou Campus. In Southeast University, 2,340 freshmen moved into the Sipailou campus this year, which is the first time in recent years that more than half of the freshmen reported to the campus.

"Walking into the campus of Dongda University, walking into Wutong Avenue, what comes to my face is the profound cultural heritage!" "Have long heard of Neusoft Meian, finally saw it today. I hope that in the future, I can also’ chew the roots and do great things’. " During the welcome period, Southeast University opened the school history museum, Mei ‘an and Wu Jianxiong Memorial Hall, and carried out campus visits to let freshmen feel the cultural atmosphere of the 120 universities in the process of searching for the source. In front of Yongquanchi, the landmark building auditorium of Dongda University, the school also organized the activity of "Freshmen Parents Say". At the scene, freshmen and parents took the stage to express their wishes and hopes and cheer for a better future together. During the activity, freshmen also wrote a wish card "to themselves after four years" and sealed it for graduation.

"Root-seeking" and "dream" are the key words on the day of registration. "We have noticed that many freshmen have special feelings for the Gulou Campus of Nantah. For example, Yang Zehao of Kaijia College, the first thing he did after reporting for the freshman training camp on August 19, was to punch in again with his photo taken with Peking University Building when he was 9 years old, thanking him for his fate with Nantah." Shi Jiahuan, deputy secretary of the Party Committee of NTU Freshmen College, told the reporter that the first year of college is a crucial period for freshmen to know the university, enter the discipline and start the future. Nanjing University has launched micro-resources for freshmen’s adaptive education, so that students can better integrate into the university, the city and the times. "Freshmen will set up their growth goals, understand the charm of the subject and find the right direction of their interests through the study of topics such as’ University and Mr. Da’,’ Adaptive Education for Freshmen’ and’ Yuhua Hong-the Power of Faith’." Shi Jiahuan said.

In the brand-new Jiangnan University Jiangyin Xiakewan Campus, the first batch of 455 "Meng Xin" settled in. Simple architectural style and water landscape with Jiangnan flavor are in the same strain as those of Jiangnan University Headquarters and Yixing Graduate School, and various banners and signs welcoming new students can be seen everywhere. Freshmen of the School of Digital Technology and Creative Design also got many "small surprises"-from brand-new visual image design and visual expression based on college English abbreviations, to specially customized canvas bags and card sets, hand-drawn maps of Xiakewan Campus in Jiangyin, and to white paper fans that can be stamped, all of which reflect the sincerity and ingenuity of the college. "This university’ meeting ceremony’ is so interesting. I will study hard and hope to have my own design works in the future." Ding Wei, a freshman majoring in digital media art, said.

Start new courses for new majors and cultivate new talents.

The reporter learned that most of the freshmen in 2024 were born in 2006, and Southeast University welcomed the post-10 students.

At the welcome scene of Dongda University, a 13-member "Xueba Group" attracted much attention. Tan Ruiqi from Fushun No.2 Middle School in Liaoning Province was the youngest of them. After three years in elementary school, two years in junior high school and two years in senior high school, Tan Ruiqi, who is only 14 years old, is the first post-10 s student in the history of Dongda University. "Learning itself is a very interesting thing. I enjoy every process of exploring the unknown, so I chose to take the college entrance examination in my second year of high school and want to invest the saved time in more creative university study." Tan Ruiqi said that when I was in primary school, portraits of scientists Qian Sanqiang and Li Siguang hung in the classroom, and I was moved after learning about their deeds. "I hope I can serve my country like them and be a useful person."

When I first entered the campus, the dream of serving the country through science and technology was already in my heart. Just entering the Intelligent Manufacturing College of Jiangnan University (Junyuan College), freshman Song Zihan saw the robot that greeted them. "I liked robots very much when I was a child, and now I am very interested in new terms such as drones and autonomous driving. The Yangtze River Delta has a strong science and technology atmosphere, and I hope that I can also participate in the production of advanced robots in the future. "

In order to cultivate future-oriented talents with new quality, many colleges and universities have implemented new training plans in the new semester. This autumn semester, the core course of artificial intelligence general education in Nanjing University, which has received much attention, officially set sail. The course is oriented to all freshmen, and through the knowledge system and training mode of deep integration of AI and various disciplines, AI literacy education is integrated into the training of top-notch innovative talents to help cultivate and develop new quality productivity. Southeast University has also created an action plan of "Artificial Intelligence+Education" for freshmen. Led by the Institute of Artificial Intelligence, the course of "Introduction to General Studies of Artificial Intelligence" has been built according to the categories of science, engineering, medicine and humanities, and an interdisciplinary virtual teaching and research section has been set up to serve the whole school’s "Artificial Intelligence +X" education, with 105 pilot projects.

In Jiangnan University, the first four colleges that settled in Jiangyin Xiakewan Campus were officially unveiled on June 7 this year, further connecting industrial transformation and local economic development. Cao Ming, dean of the School of Digital Technology and Creative Design of the school, said that in order to meet the new needs of the industry, the design discipline of the school is being adjusted around intelligent technology and intelligent interaction. "For example, the curriculum design of digital media art majors is more inclined to interactive media and virtual interaction. Fashion design majors integrate smart wearable devices into teaching. In the overall curriculum system, the college will also join artificial intelligence courses for freshmen. " (Yang Pinping, Xie Shihan, Ye Zhen)

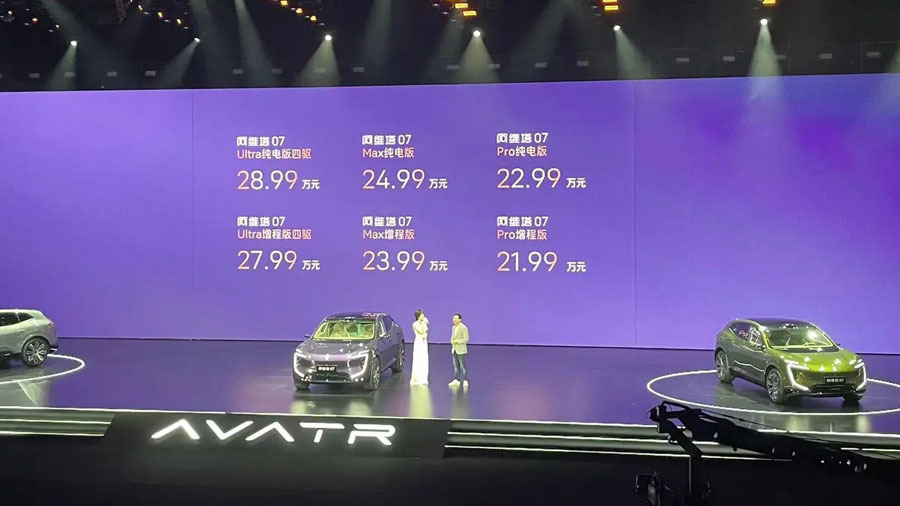

Extreme Yue 07 is a new model jointly launched by Geely and Baidu. It is based on the vast architecture of Geely SEA, focusing on intelligent technology, equipped with a brand-new end-to-end perception model, and optionally equipped with the official version of advanced intelligent driving 2.0. This is a pure visual intelligent driving scheme, and Baidu has polished a lot of time on this intelligent driving scheme.

Extreme Yue 07 is a new model jointly launched by Geely and Baidu. It is based on the vast architecture of Geely SEA, focusing on intelligent technology, equipped with a brand-new end-to-end perception model, and optionally equipped with the official version of advanced intelligent driving 2.0. This is a pure visual intelligent driving scheme, and Baidu has polished a lot of time on this intelligent driving scheme. Adhering to the design concept of Less is more, the shape of the new car is really good. The front of the car is a closed grille with a penetrating LED daytime running light strip, and the light groups on both sides are designed in an inverted T shape. The upper and lower parts are designed with intelligent interactive light groups, while the middle is a horizontally arranged LED light source with lenses. The trapezoidal air intake is below the front of the car. The whole front face is simple but not simple, and it has a good sense of movement with the clamshell cover.

Adhering to the design concept of Less is more, the shape of the new car is really good. The front of the car is a closed grille with a penetrating LED daytime running light strip, and the light groups on both sides are designed in an inverted T shape. The upper and lower parts are designed with intelligent interactive light groups, while the middle is a horizontally arranged LED light source with lenses. The trapezoidal air intake is below the front of the car. The whole front face is simple but not simple, and it has a good sense of movement with the clamshell cover. The side of the car body is designed with a sliding back coupe style, and the roof line is smooth, with no door handle (pressing the button to open the electric door), hidden water tangent and hidden B-pillar, no obvious waist line, and the door cambered transition, which brings a low drag coefficient of 0.198Cd. The rear part is designed with a hatchback tailgate and a super-running wide-body rear shoulder, with a through taillight group, and the two sides are made into a split style, which is very recognizable.

The side of the car body is designed with a sliding back coupe style, and the roof line is smooth, with no door handle (pressing the button to open the electric door), hidden water tangent and hidden B-pillar, no obvious waist line, and the door cambered transition, which brings a low drag coefficient of 0.198Cd. The rear part is designed with a hatchback tailgate and a super-running wide-body rear shoulder, with a through taillight group, and the two sides are made into a split style, which is very recognizable. The interior is made in a minimalist style. The center console is equipped with a 35.6-inch penetrating screen, with a D-shaped dual-spoke, and a U-shaped semi-spoke is optional for a limited time. All the buttons and knobs in the car are simplified, and only two rollers and four button indicators are reserved on the steering wheel, which are used to control the left and right turn signals, wipers and lighting functions respectively. Just like Tesla, the gears are integrated in the screen, and the sliding shift mode is adopted.

The interior is made in a minimalist style. The center console is equipped with a 35.6-inch penetrating screen, with a D-shaped dual-spoke, and a U-shaped semi-spoke is optional for a limited time. All the buttons and knobs in the car are simplified, and only two rollers and four button indicators are reserved on the steering wheel, which are used to control the left and right turn signals, wipers and lighting functions respectively. Just like Tesla, the gears are integrated in the screen, and the sliding shift mode is adopted. At present, this design is a trend, but whether it is good or not, for drivers who are used to dialing the lever to light, it will be unaccustomed to suddenly changing to the button type, especially when the steering angle of the steering wheel is larger in the turning state, so it is difficult to distinguish the left and right control of the light. If it is changed to a semi-spoke steering wheel, it will not be difficult to use it without turning back, but this kind of steering wheel also needs to be adapted, especially when the vehicle is moving at low speed or turning around.

At present, this design is a trend, but whether it is good or not, for drivers who are used to dialing the lever to light, it will be unaccustomed to suddenly changing to the button type, especially when the steering angle of the steering wheel is larger in the turning state, so it is difficult to distinguish the left and right control of the light. If it is changed to a semi-spoke steering wheel, it will not be difficult to use it without turning back, but this kind of steering wheel also needs to be adapted, especially when the vehicle is moving at low speed or turning around. The length of the car is 4,953 mm, the width is 1,989 mm, the height is 1,480 mm, and the wheelbase of the new car is 3,013 mm. Although it is a coupe body posture, there is no problem in the interior space. Passengers with a height of 175 cm have more than one punch in the front and rear rows, and more than two punches in the leg space when sitting in the second row.

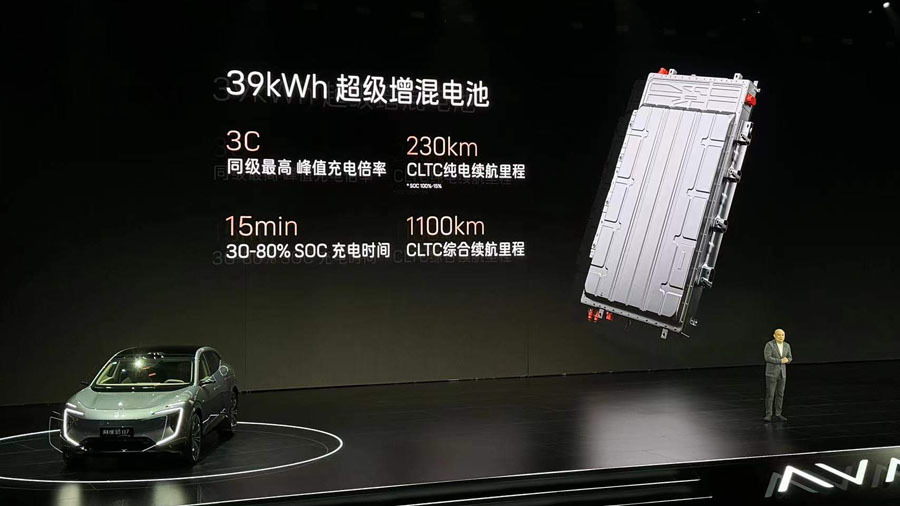

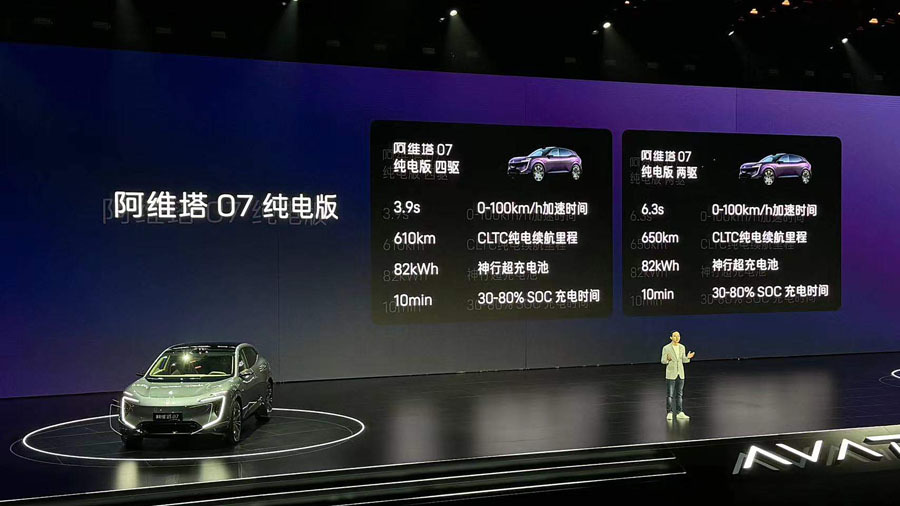

The length of the car is 4,953 mm, the width is 1,989 mm, the height is 1,480 mm, and the wheelbase of the new car is 3,013 mm. Although it is a coupe body posture, there is no problem in the interior space. Passengers with a height of 175 cm have more than one punch in the front and rear rows, and more than two punches in the leg space when sitting in the second row. In terms of power, the new car has two single-motor models and one dual-motor model. The maximum power of a single motor is 200 kW, and the zero-hundred acceleration is 6.9 seconds and 6.5 seconds respectively, so the power is sufficient. The version uses the first 230 and the last 300 kW motors, and the fastest zero-hundred acceleration is 3.5 seconds. It is equipped with 71.4/100/93.4 kWh battery packs, and the corresponding cruising range is 660/880/770 respectively. Support fast charging, but all models do not provide slow charging port, which is a bit inappropriate and supports external discharge.

In terms of power, the new car has two single-motor models and one dual-motor model. The maximum power of a single motor is 200 kW, and the zero-hundred acceleration is 6.9 seconds and 6.5 seconds respectively, so the power is sufficient. The version uses the first 230 and the last 300 kW motors, and the fastest zero-hundred acceleration is 3.5 seconds. It is equipped with 71.4/100/93.4 kWh battery packs, and the corresponding cruising range is 660/880/770 respectively. Support fast charging, but all models do not provide slow charging port, which is a bit inappropriate and supports external discharge.